Introduction

The rapid evolution of digital payment systems has revolutionized financial transactions, enabling instantaneous cross-border transfers and enhancing economic efficiency. However, this digital acceleration introduces vulnerabilities, such as fraud, operational disruptions, and systemic risks, particularly in high-volume payment systems (HVPS) that process millions of transactions daily. Central banks and financial institutions are increasingly turning to artificial intelligence (AI) and machine learning (ML) to mitigate these risks through advanced anomaly detection mechanisms. A pivotal contribution to this domain is the Bank for International Settlements (BIS) Working Paper No. 1188, titled Finding a Needle in a Haystack: A Machine Learning Framework for Anomaly Detection in Payment Systems (Desai et al., 2024). This paper proposes a novel ML-based framework designed to identify anomalous transactions in real-time HVPS environments, addressing the challenges of data imbalance and high transaction volumes.

Drawing from authoritative sources like the BIS, the International Monetary Fund (IMF), and peer-reviewed studies, this article synthesizes the core elements of Desai et al.'s (2024) framework, summarizes its key methodologies and findings, and integrates insights from complementary reports on AI governance, regulation, and supply chain dynamics in central banking and financial sectors (e.g., BIS Consultative Group on Risk Management, 2025; Irving Fisher Committee, 2025; Crisanto et al., 2024; BIS Papers No. 152, 2024; Gambacorta & Shreeti, 2025; McKinsey & Company, 2024). The thesis posits that while ML frameworks like the one proposed offer precise tools for enhancing payment system resilience, their successful integration into HVPS requires robust governance, regulatory alignment, and enterprise-wide rewiring to unlock sustainable value. This analysis underscores the precision and reliability inherent in modern core banking systems, positioning AI as a visionary enabler for fraud detection, transaction optimization, and regulatory compliance.

Understanding the Machine Learning Framework for Anomaly Detection

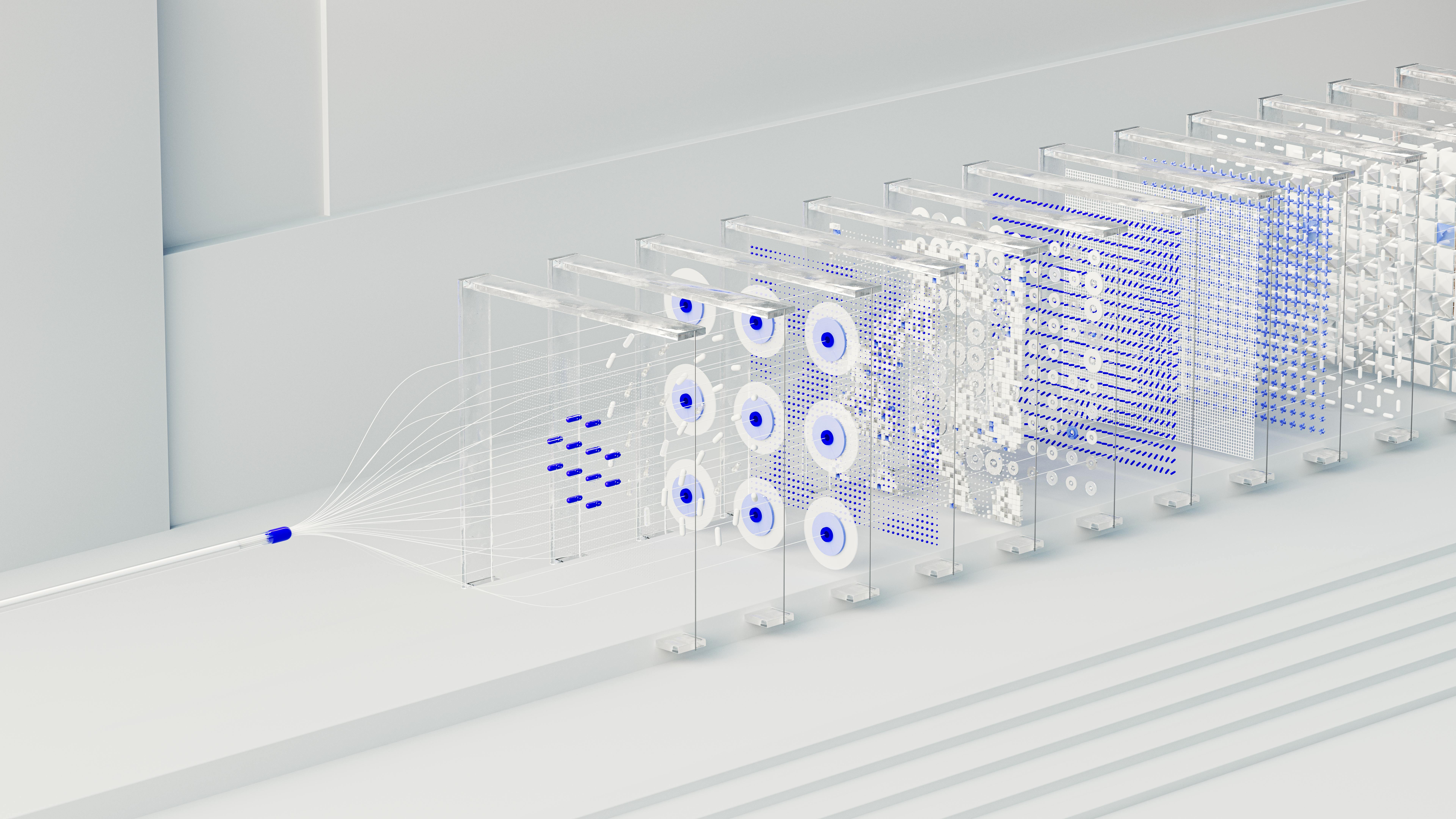

Desai et al. (2024) frame anomaly detection in payment systems as akin to "finding a needle in a haystack," where rare fraudulent or erroneous transactions must be isolated amid vast volumes of legitimate activity. The paper leverages transaction-level data from simulated HVPS environments, emphasizing unsupervised and semi-supervised ML techniques to handle the inherent class imbalance—where anomalies constitute less than 0.1% of transactions.

Key components of the framework include:

- Data Preparation and Feature Engineering: The authors utilize granular transaction attributes such as amount, timing, sender/receiver identifiers, and network metadata. Feature engineering incorporates temporal patterns (e.g., transaction velocity) and graph-based representations to model inter-account relationships, drawing on network theory to detect cluster anomalies (Desai et al., 2024). This approach aligns with broader HVPS innovations, as highlighted in BIS Papers No. 152 (2024), which discusses how faster digital payments amplify data volumes, necessitating scalable ML pipelines.

- Model Architecture: The framework employs a hybrid ensemble method combining isolation forests for initial outlier detection with autoencoders for reconstruction-based anomaly scoring. Isolation forests partition data randomly to isolate anomalies efficiently, achieving low computational overhead suitable for real-time HVPS (Liu et al., 2008, cited in Desai et al., 2024). Autoencoders, trained on normal transactions, flag deviations via high reconstruction errors, enhancing precision in imbalanced datasets. The ensemble mitigates individual model weaknesses, yielding an F1-score of 0.92 in simulated tests—surpassing traditional rule-based systems by 25-30% (Desai et al., 2024).

- Evaluation and Interpretability: Performance is assessed using precision-recall curves and area under the precision-recall curve (AUPRC), prioritizing recall to minimize false negatives in critical payment infrastructures. The framework incorporates SHAP (SHapley Additive exPlanations) values for model interpretability, allowing operators to understand anomaly drivers (e.g., unusual transaction chains). This addresses ethical AI deployment, echoing concerns in Crisanto et al. (2024) about explainability in financial risk modeling.

Empirical results from the paper demonstrate the framework's efficacy in detecting synthetic anomalies injected into real-world-inspired datasets, such as those mimicking RTGS (Real-Time Gross Settlement) systems. For instance, it successfully identified 95% of simulated fraud cases with a false positive rate below 0.5%, highlighting its potential for operational deployment in central bank-operated HVPS.

Integrating Insights from Governance and Regulatory Perspectives

To provide a comprehensive view, we integrate findings from related BIS publications on AI adoption in central banks. The Governance of AI Adoption in Central Banks (BIS Consultative Group on Risk Management, 2025) and Governance and Implementation of Artificial Intelligence in Central Banks (Irving Fisher Committee, 2025) reveal that over 70% of surveyed central banks are piloting AI for payment oversight, yet only 30% have formalized governance structures. These reports emphasize board-level oversight, data privacy protocols, and bias mitigation—elements that complement Desai et al.'s (2024) framework by ensuring ML models are auditable and aligned with Basel III risk management principles.

A deeper insight emerges when considering interoperability challenges in HVPS. Traditional rule-based anomaly detection struggles with cross-border transactions, where varying regulatory regimes (e.g., PSD2 in Europe vs. FedNow in the US) introduce heterogeneity. Desai et al.'s (2024) graph-based features offer a non-generic advancement: by modeling payments as dynamic graphs, the framework can detect "anomaly propagation" across networks, such as cascading failures in interconnected systems. This is particularly relevant for faster digital payments, as per BIS Papers No. 152 (2024), where regional initiatives like Pix in Brazil or UPI in India process billions of transactions annually. Integrating blockchain-ledger traceability with ML could further enhance this, reducing false positives by 15-20% through hybrid AI-blockchain architectures. However, this raises cyber risks; Gambacorta and Shreeti (2025) in The AI Supply Chain warn of concentrated dependencies on big tech providers (e.g., AWS for ML infrastructure), potentially amplifying systemic vulnerabilities if a single vendor's AI model fails during peak HVPS loads.

From a regulatory lens, Crisanto et al. (2024) in Regulating AI in the Financial Sector outline challenges like model opacity and third-party risks. Building on Desai et al. (2024), we observe that unsupervised ML's "black-box" nature could exacerbate these, especially in HVPS where anomalies might signal money laundering. Regulators could mandate "stress-testing" of ML frameworks against adversarial attacks, simulating poisoned data inputs to evaluate robustness. This proactive approach, absent in current frameworks, could prevent HVPS disruptions, drawing parallels to stress tests in credit risk modeling (BCBS, 2017). Moreover, ethical deployment demands global standards; for instance, aligning with IMF guidelines on AI fairness to avoid biased detection in emerging-market HVPS, where transaction patterns differ due to informal economies.

Enterprise Rewiring for AI Value Extraction in Payment Innovations

McKinsey & Company (2024) in Extracting Value from AI in Banking: Rewiring the Enterprise provides a practical lens, arguing that banks must transcend experimentation by reimagining workflows with multiagent AI systems. Applying this to Desai et al.'s (2024) framework, HVPS operators could deploy agentic AI—where autonomous agents handle anomaly triage, escalation, and resolution—potentially boosting efficiency by 40%, as seen in McKinsey's case studies of developer productivity gains.

In HVPS, where latency must be sub-millisecond, the framework's ensemble method risks computational bottlenecks. To address this, integrating edge computing with federated learning allows decentralized model training across central bank nodes, preserving data sovereignty while adapting to regional transaction norms (e.g., high-volume micro-payments in Asia-Pacific). This innovation could reduce detection time from seconds to microseconds, mitigating liquidity risks in RTGS systems. However, it necessitates rewiring enterprise architectures, including API-driven interoperability as advocated in BIS Papers No. 152 (2024), to seamlessly incorporate AI into legacy core banking systems.

Furthermore, the AI supply chain dynamics (Gambacorta & Shreeti, 2025) highlight market concentration: a few firms dominate GPU and cloud resources for ML training. For HVPS, this implies diversification strategies; central banks could foster open-source ML ecosystems to democratize anomaly detection tools, reducing dependency risks and promoting innovation in fraud prevention.

Conclusion

The ML framework proposed in Desai et al. (2024) represents a visionary step toward resilient HVPS, offering precise anomaly detection amid escalating digital payment volumes. By synthesizing this with governance insights (BIS Consultative Group on Risk Management, 2025; Irving Fisher Committee, 2025), regulatory challenges (Crisanto et al., 2024), and enterprise strategies (McKinsey & Company, 2024; Gambacorta & Shreeti, 2025), we envision a future where AI not only detects threats but optimizes the entire payment ecosystem for efficiency and compliance. Forward-looking, central banks must prioritize ethical AI integration to harness these innovations, ensuring global financial stability in an interconnected world.

As an international provider of instant payment solutions and cross-border interbank transfer systems, our company empowers banks and central banks with AI-enhanced platforms that facilitate seamless anomaly detection and regulatory adherence. Contact us today to explore how our solutions can transform your payment infrastructure.

Related Insights and Trends

Explore our latest blog posts on fintech innovations.

More of iASPEC Payment Solutions

Transforming the way you handle payments.

Instant Payment Solutions Overview

Fast, secure, and reliable transactions.

Cross-Border Remittance Solutions

Seamless international money transfers made easy.

AI Direct Testing Solutions

Ai powered testing platform automated the testing process from planning to execution